You served your country. Now it is time to build the home you actually want, in the city you call home, with the benefit you already earned.

At Builders Group Construction (BGC), we build custom homes for veterans in Dayton using VA financing. We know the VA process inside and out. We handle the paperwork, permits, and details so you can focus on your design.

In most cases, there’s no down payment. Just a clear path to a home that’s built for you.

Most veterans don’t realize this, but you can use your VA loan benefit to build a brand new home, not just buy one. VA loan new construction is a real option, and for many people, it means getting exactly what they want instead of settling.

The thing is, not every builder is set up for VA loan new construction. You need someone who understands the requirements, works with the right lenders, and can keep everything moving without delays.

That’s where we come in. At BGC, we help veterans in Dayton build custom homes using a VA loan to build a house. We keep the process simple, walk you through each step, and make sure nothing slips through the cracks.

VA Loan Requirements for Building a Home

Before you start, it helps to know what the VA looks for. Here are the main VA construction loan requirements:

Credit Score: Most VA lenders want a credit score of at least 620. Some lenders may accept lower scores. Ask your lender what their minimum is.

Certificate of Eligibility (COE): This document proves you qualify for VA benefits. You can get it through your lender or directly through the VA.

VA Approved Builder: The builder must be registered with the VA. If you build with a non-approved contractor, the VA will not back the loan.

Approved Construction Plans: The VA requires detailed plans before approving the loan. Plans must show the home will meet VA minimum property requirements.

VA Appraisal: An appraiser will review your plans and estimate the value of the finished home. The loan amount is based on this estimate.

We help you get all of this in place upfront so you don’t run into delays later. If you want more background, the Consumer Financial Protection Bureau has a helpful breakdown of VA loan basics.

Veterians Affairs Loan

Can You Build a Home With a VA Loan?

Yes, you can build a home with a VA loan.

A lot of people assume VA loans only apply to existing homes, but that’s not the case. A VA construction loan allows you to finance the build of a brand new home. Once construction is complete, the loan converts into a standard VA mortgage.

You still get the benefits you earned. No down payment in most cases, no private mortgage insurance, and competitive rates.

To build a house with a VA loan, you’ll need a few key pieces in place:

A VA approved builder (like BGC)

A lender who offers VA construction loans

Approved construction plans and permits

A VA appraisal of the planned home

We help you work through all of this. Our team connects you with trusted local lenders and walks you through each step.

Before anything else, you’ll want to confirm your VA loan eligibility. That means getting your Certificate of Eligibility (COE) and working with a VA-approved lender to get pre-approved. You will want to speak to someone who specializes in VA construction loans.

STEP 2

Choose a VA Approved Builder

This is where we come in. Once you are pre-approved, you select your builder. When you choose BGC, you’re working with a team that already understands VA loan new construction requirements. That means fewer delays, fewer surprises, and a much smoother process overall.

STEP 3

Design Your Home & VA Approvals

We’ll sit down with you and go through your options, floor plans, layouts, finishes, all of it. You choose what works for your family and your budget, and we make sure everything lines up with VA appraisal standards so there are no issues later.

STEP 4

The Construction will begin

Once everything is approved and permits are in place, we get started. We keep you updated throughout the build so you’re not wondering what’s going on. You’ll see steady progress, and we stay on top of timelines to keep things moving toward your move-in date.

STEP 5

Move Into Your New Home

When construction is complete, your VA construction loan converts to a permanent VA mortgage. You get the keys. You move in. And you’re in a brand new home that was built around your needs, not someone else’s.

Why Veterans Choose Us as Their VA Approved Builder in Dayton

There are plenty of builders in Dayton, so why do veterans keep choosing Builders Group Construction? It comes down to experience and how we handle the process.

We know VA construction loans. We have worked through the VA process many times. We understand what lenders need, what the VA requires, and how to keep your project moving without delays.

We are licensed and insured. You are making one of the biggest investments of your life. You need a builder you can trust. BGC is fully licensed and insured in Ohio.

We are local. We build in Dayton and the surrounding area. We know the neighborhoods, the permit offices, and the local market. You are not dealing with a company based somewhere else.

We are transparent about pricing. No hidden fees. No last-minute add-ons. We give you a clear picture of costs before we start.

We respect your service. Veterans get straight answers and honest communication from our team.

VA Loan Requirements for Building a Home

Before you start, it helps to know what the VA looks for. Here are the main VA construction loan requirements:

Credit Score: Most VA lenders want a credit score of at least 620. Some lenders may accept lower scores. Ask your lender what their minimum is.

Certificate of Eligibility (COE): This document proves you qualify for VA benefits. You can get it through your lender or directly through the VA.

VA Approved Builder: The builder must be registered with the VA. If you build with a non-approved contractor, the VA will not back the loan.

Approved Construction Plans: The VA requires detailed plans before approving the loan. Plans must show the home will meet VA minimum property requirements.

VA Appraisal: An appraiser will review your plans and estimate the value of the finished home. The loan amount is based on this estimate.

We help you get all of this in place upfront so you don’t run into delays later. If you want more background, the Consumer Financial Protection Bureau has a helpful breakdown of VA loan basics.

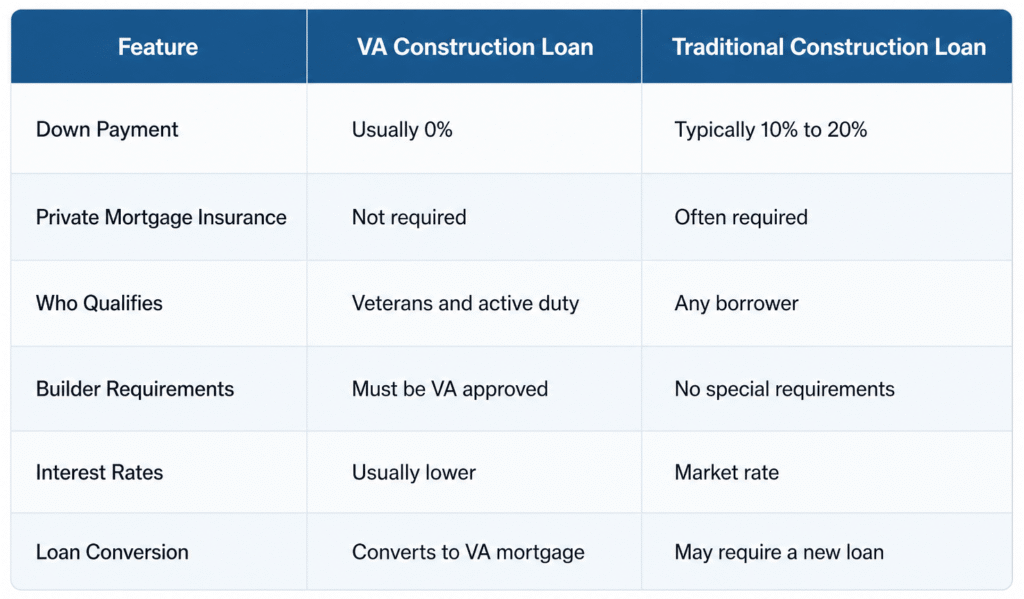

VA Construction Loans vs Traditional Construction Loans

Not sure how a VA construction loan compares to a regular construction loan? Here is a quick breakdown.

For most veterans, a VA construction loan is the better option. You save money upfront and usually get better terms overall.

Ready to Build? Talk to a VA Approved Builder in Dayton Today

You earned your VA benefit. Use it to build a home that fits your life. BGC is here to make that happen. We will walk you through every step, connect you with the right lenders, and build a home you will love.

Call us today or fill out our contact form to get started.

Yes. Veterans can build a brand new home using a VA construction loan. You work with a VA approved builder and a VA-approved lender. When the home is done, the loan converts to a standard VA mortgage.

Do all builders accept VA loans?

No. Only builders who are registered with the VA can build homes using VA financing. If your builder is not VA approved, your loan will not be backed by the VA.

How long does it take to build a home with a VA loan?

Most new construction homes take 6 to 12 months to build. The timeline depends on the size of the home, the design, and how quickly permits are approved.

Is a down payment required for a VA construction loan?

In most cases, no down payment is required. That is one of the biggest benefits of using a VA loan to build a house.

What is a Certificate of Eligibility?

A Certificate of Eligibility (COE) is a document from the VA that confirms you qualify for VA loan benefits. Your lender can help you get it, or you can request it directly through the VA.

Can my spouse use a VA loan to build a home?

Surviving spouses of veterans may qualify for VA loan benefits in some cases. A VA-approved lender can help you confirm eligibility.

What happens if the home appraises for less than the construction cost?

If the appraisal comes in low, you may need to adjust the plans or cover the difference. We work with you upfront to design a home that is likely to appraise at or above the construction cost.