If you served in the military, you already earned a benefit that most people don’t know about. You can use your VA loan to build a brand new home, not just buy one. That means no down payment in most cases, no private mortgage insurance, and a home built exactly the way you want it.

This guide explains how VA construction loans work in Dayton, step by step. If you are ready to start building, Builders Group Construction is a VA-approved builder in Dayton who can walk you through the entire process.

What Is a VA Construction Loan?

A VA construction loan lets eligible veterans and active-duty service members finance the construction of a new home. The Department of Veterans Affairs backs the loan, which gives lenders confidence to offer better terms.

Unlike a standard VA loan used to buy an existing home, a construction loan covers the cost of building from the ground up. Once the home is finished, the loan converts into a permanent VA mortgage. That’s what’s called a construction-to-permanent loan.

The home must be your primary residence. You can’t use this loan to build a home or rental property.

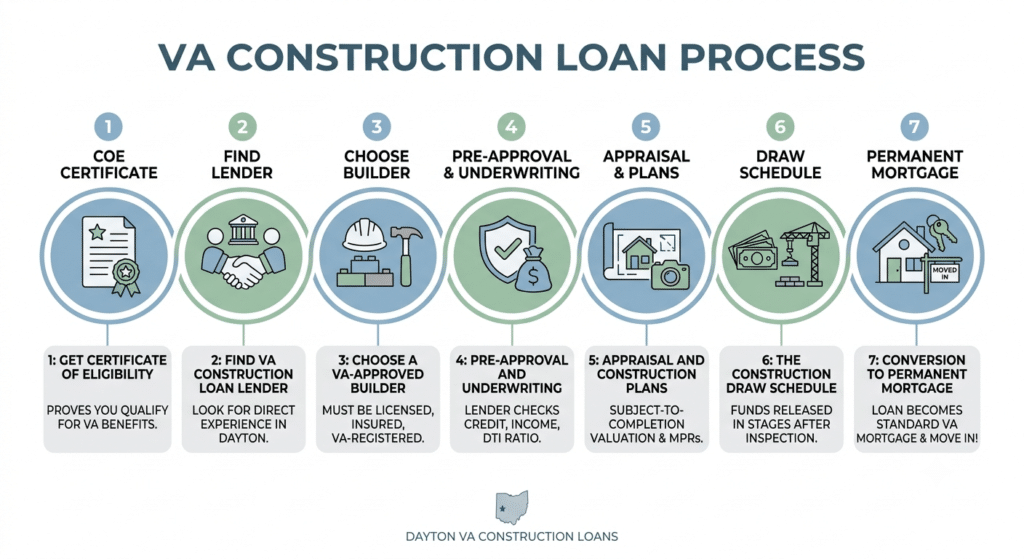

How Do VA Construction Loans Work in Dayton?

Here is the process broken down simply.

Step 1: Get Your Certificate of Eligibility

Your Certificate of Eligibility, or COE, proves to lenders that you qualify for VA benefits. You can get it through your lender or directly through the VA website. Most lenders will help you pull this quickly. Without it, the loan process can’t move forward.

Step 2: Find a VA Construction Loan Lender in Dayton

Not every lender offers VA construction loans. It’s a more complex product, so fewer banks and credit unions handle it. Look for lenders with direct experience in VA new construction financing, not just standard VA purchase loans. Ask them how many VA construction loans they’ve closed in the past year. That answer tells you a lot.

The Consumer Financial Protection Bureau has helpful resources to understand your mortgage rights and how to compare lenders.

Step 3: Choose a VA-Approved Builder

This step is critical. The VA requires that your builder be registered and approved. If you work with a builder who isn’t VA-approved, the loan won’t be backed by the VA.

A VA-approved builder must be licensed, insured, and registered directly with the VA. Builders Group Construction meets all of these requirements. Our team handles the registration paperwork and works directly with your lender to keep things moving without delays.

Step 4: Pre-Approval and Underwriting

Your lender will look at your credit score, income, debt-to-income ratio, and residual income. Most VA lenders want a credit score of at least 620. Residual income is the money left over after all monthly bills are paid. The VA uses this number to make sure you can afford the home long-term.

Get your documents ready early. Pay stubs, tax returns, and bank statements are standard.

Step 5: Appraisal and Construction Plans

Before the loan is approved, the VA requires a subject-to-completion appraisal. An appraiser reviews your blueprints and estimates what the finished home will be worth. The loan amount is based on that number.

Your plans must also show the home will meet VA Minimum Property Requirements. BGC helps clients remodeling homes that meet these standards from the start, which avoids delays later.

Step 6: The Construction Draw Schedule

This is how money is released during the build. Rather than getting one lump sum, funds are released in stages called draws. Each draw happens after a completed phase is inspected and approved.

A typical draw schedule looks like this:

| Phase | Payment Released |

| Foundation complete | Draw 1 |

| Framing complete | Draw 2 |

| Rough mechanical done | Draw 3 |

| Drywall and interior | Draw 4 |

| Final completion | Draw 5 |

Inspections happen before each draw is released. This protects both you and the lender.

Step 7: Conversion to Permanent Mortgage

When construction is complete, your loan converts to a standard VA mortgage. A final inspection confirms the home is finished and meets all requirements. Then you get the keys and move in. Your monthly payments on the permanent loan start from there.

One-Time Close vs Two-Time Close

| Feature | One-Time Close | Two-Time Close |

| Number of closings | One | Two |

| Closing costs | Lower | Higher |

| Rate lock | Earlier | Later |

| Process | Simpler | More complex |

Most veterans prefer the one-time close option. You sign once, lock your rate, and avoid paying closing costs twice. BGC works with lenders who specialize in one-time close VA construction loans.

VA Construction Loan Requirements

Here is a quick checklist of what you need to qualify:

- Active-duty, veteran, or eligible surviving spouse status

- Valid Certificate of Eligibility

- Credit score of 620 or higher (varies by lender)

- Acceptable debt-to-income ratio

- Sufficient residual income

- VA-approved builder

- Approved construction plans and blueprints

- Subject-to-completion appraisal

Can You Buy Land With a VA Construction Loan?

In some cases, yes. Certain lenders allow you to include land purchase costs in a VA construction loan. The land must be part of the overall home construction project. Not every lender offers this, so ask specifically about VA land and construction financing when you shop lenders.

Common Costs to Know

Here are fees to plan for:

- VA funding fee (typically 1.25% to 3.3% of the loan amount)

- Appraisal fee

- Construction draw inspection fees

- Builder deposit

- Interest reserve account (covers interest during the build)

The good news is there’s no PMI and usually no down payment. That saves a significant amount compared to conventional construction loans.

Why VA Construction Loans Are Harder to Get

VA construction loans require more work from lenders. The underwriting is more involved, builder registration adds a step, and construction risk is higher than a standard purchase. Fewer lenders offer this product as a result.

The fix is simple. Work with a builder and lender who already know the process. BGC has worked through VA construction financing many times. Our design-build remodeling and construction services are built around keeping clients informed and on track.

VA Construction Loan Timeline

| Phase | Estimated Time |

| Pre-approval | 1 to 2 weeks |

| Builder approval | 2 to 4 weeks |

| Underwriting | 2 to 3 weeks |

| Construction | 6 to 12 months |

| Final conversion | 1 to 2 weeks |

Plan for the full process to take about 8 to 14 months from start to move-in.

Frequently Asked Questions

Do VA construction loans require a down payment?

In most cases, no. That’s one of the biggest benefits of using your VA benefit to build.

What credit score do I need?

Most lenders want at least 620. Some may go lower depending on other factors.

Can I use any builder?

No. The builder must be registered with the VA. BGC serves Dayton and nearby cities including Beavercreek, Kettering, and Tipp City.

How long does construction take?

Most new builds take 6 to 12 months depending on size and design.

Is a VA construction loan worth it?

For most veterans who want a custom home, yes. No down payment and no PMI make it one of the most affordable ways to build.

Ready to build? Call BGC at 937-800-4409 or request your free consultation at bgcnow.us.