Many veterans do not realize their VA loan benefit works on more than a single-family home. You can use a VA loan to buy a duplex, triplex, or fourplex in Dayton with no down payment, as long as you live in one of the units as your primary residence.

This opens up a real opportunity. You buy a home, live in one unit, and rent the others. The rental income helps offset your mortgage. That is the core of what people call house hacking, and the VA loan makes it more accessible than any other loan program available to veterans.

If you are planning to build a multifamily home in Dayton rather than buy an existing one, Builders Group Construction is a VA-approved builder that works with veterans through the full construction and financing process.

Can You Use a VA Loan for a Multifamily Property?

Yes. VA loans allow eligible veterans and active-duty service members to purchase properties with up to four residential units. The key requirement is that you must occupy one unit as your primary residence.

This is not an investment loan in the traditional sense. The VA program is built around helping veterans secure stable housing. The fact that you can rent out the other units is a benefit of the structure, not the primary purpose. If you are still exploring how VA construction financing works from the ground up, our guide on how VA construction loans work covers the full process.

Eligible Property Types

The VA covers these multifamily property types:

- Duplex: 2 units

- Triplex: 3 units

- Fourplex: 4 units

Anything with five or more units falls outside what a VA loan can finance. Those properties require commercial financing, regardless of whether you plan to live in one unit.

Duplex vs Triplex vs Fourplex

| Property Type | Units | Rental Units Available | Self-Sufficiency Test Required |

| Duplex | 2 | 1 | No |

| Triplex | 3 | 2 | Often yes |

| Fourplex | 4 | 3 | Often yes |

The more units, the more documentation lenders typically require. Triplexes and fourplexes also trigger additional underwriting requirements that duplexes do not.

VA Owner-Occupancy Requirements

Primary Residence Rules

The VA requires that the property be your primary residence. You can’t use a VA loan to buy a multifamily property purely as a rental investment. You must genuinely intend to live there, and your file needs to support that intent.

The 60-Day Move-In Expectation

Most lenders expect you to move into your unit within 60 days of closing. There are exceptions for active military situations, ongoing repairs, or other documented circumstances, but 60 days is the standard expectation lenders work from.

How Long Must You Live There?

The VA itself doesn’t set a specific minimum time you must live in the property before moving out. However, many lenders apply a 12-month overlay as a practical benchmark. Moving out quickly after closing in a way that looks planned can create questions about whether your occupancy intent was genuine at the time you applied.

If you receive PCS orders or are deployed, that is a legitimate reason to vacate. The VA understands military life requires moves. What matters is that your intent was honest when you signed your loan documents.

Rental Income Rules for VA Multifamily Loans

Using Rental Income to Qualify

Rental income from the non-owner units can help you qualify for a larger loan. However, lenders do not count the full projected rent. Most use 75% of the appraiser’s estimated market rent for each unit. That 25% discount accounts for vacancy periods and maintenance costs.

Here is why this matters practically. If the market rent on your two rental units is $1,800 each per month, the lender counts $1,350 per unit, or $2,700 total, not the full $3,600.

If your deal only works using 100% of projected rent, it is too tight for underwriting and likely too risky in practice. Understanding VA loan affordability before you make an offer helps you run these numbers accurately from the start.

Landlord Experience Requirements

Many lenders require documentation of prior property management experience before they will credit rental income toward your qualification. They want to see that you have a reasonable track record of managing tenants and maintenance.

If you don’t have landlord experience, some lenders will accept a documented property management plan or a contract with a property management company as a substitute.

Lease Agreement Documentation

If the units are already occupied, gather leases, rent rolls, and proof of deposits early. Underwriting can’t count income it can’t document, and late paperwork creates rework that delays closing. If units are vacant, the appraiser’s market rent estimate becomes the reference point.

Understanding the VA Self-Sufficiency Test

When It Applies

The self-sufficiency test is a lender overlay that commonly appears on three and four-unit purchases. It’s not an official VA rule, but many lenders apply it on larger multifamily files.

The test requires that the net rental income from the non-owner units cover the full monthly mortgage payment. If it doesn’t, the lender may require additional income, larger reserves, or may decline the loan.

How Rental Income Is Calculated

The lender takes the appraiser’s market rent estimate, applies a 75% factor for vacancy and expenses, and compares the result to your monthly principal, interest, taxes, and insurance payment.

Example:

| Item | Amount |

| Market rent per non-owner unit | $1,500 |

| Two non-owner units combined | $3,000 |

| After 75% factor | $2,250 |

| Monthly PITI payment | $2,100 |

| Self-sufficiency result | Passes |

If the rent after the 75% factor falls below the PITI payment, the property fails the self-sufficiency test with that lender.

Why Some Properties Fail

Properties fail when market rents are low relative to purchase price, when the appraiser’s rent estimate comes in below what the seller claims, or when PITI is higher than expected due to taxes or insurance. Run this math conservatively before making an offer.

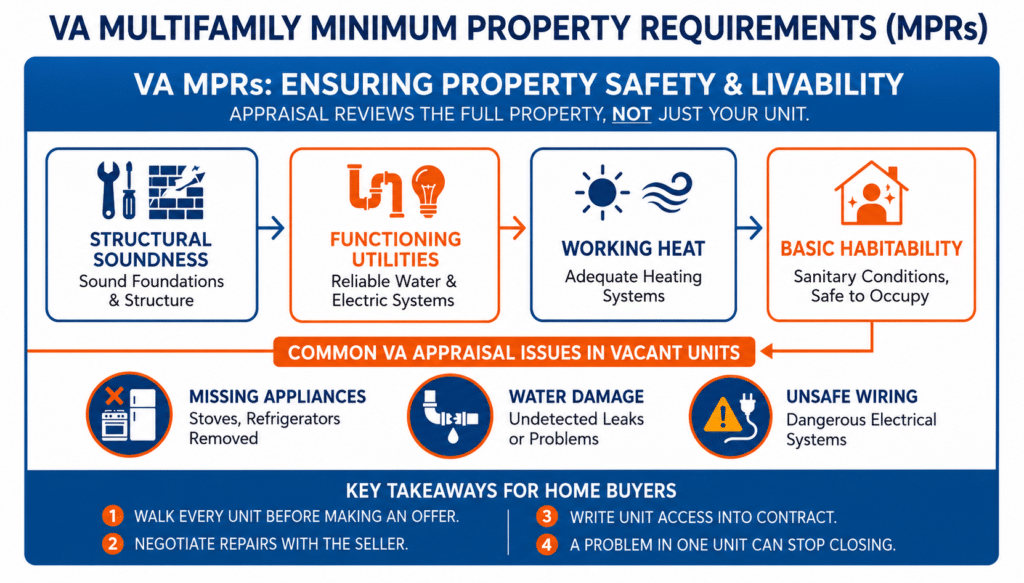

VA Minimum Property Requirements for Multifamily

Safety and Livability Standards

The VA appraisal reviews the entire property, not just the unit you plan to occupy. Every unit must meet VA Minimum Property Requirements, or MPRs. These cover structural soundness, functioning utilities, safe electrical systems, working heat, and basic habitability.

A problem in a vacant unit can stop your closing just as quickly as a problem in your own unit. The VA appraisal is designed to protect the veteran and ensure the property is safe, sound, and sanitary across the full structure.

Common Appraisal Issues

Vacant units are where problems hide. Sellers sometimes remove appliances or skip repairs in units they consider empty. Missing stoves, broken heating systems, water damage, and unsafe wiring in vacant units are common reasons VA appraisals add repair conditions.

Walk every unit before making an offer when possible. Finding problems before the appraisal lets you negotiate repairs with the seller rather than scrambling mid-underwriting. Write unit access requirements into your contract so tenants cannot control your closing timeline. If you are building rather than buying, working with a VA-approved builder in Dayton ensures every unit meets MPRs from day one.

Financial Requirements for Multifamily VA Loans

Debt-to-Income Ratio

The VA uses 41% DTI as a general benchmark. Going above that isn’t an automatic disqualification, especially when residual income is strong, but multifamily files already carry more complexity, so staying near or below 41% makes underwriting smoother.

Cash Reserve Requirements

This is where multifamily VA loans differ significantly from single-family purchases. Many lenders require 3 to 6 months of full PITI payments in verified liquid reserves when rental income is used to qualify. The reasoning is straightforward. Vacancies, repairs, and tenant turnover create cash flow interruptions, and lenders want to see that you can cover the mortgage during those periods.

Confirm the reserve requirement with your lender before going under contract. Learning late that you need six months of reserves when you only have two is a common reason for last-minute problems.

Residual Income Rules

Residual income is the money left over after all monthly expenses are paid. The VA uses regional thresholds based on family size. Exceeding the threshold by 20% or more is a strong compensating factor, especially on files with more complexity. For multifamily files, strong residual income can help offset higher DTI or marginal credit scores.

VA Loan Limits and Multifamily Homes

Loan limits matter mainly when you have partial entitlement. If you have full entitlement, the VA does not impose a loan cap, but you still must qualify through income and appraisal. For a full breakdown of how entitlement works, see our VA entitlement explained guide.

Here are the 2026 standard county limits for multifamily properties:

| Property Type | 2026 Standard Limit |

| Duplex | $1,066,250 |

| Triplex | $1,288,800 |

| Fourplex | $1,601,750 |

Partial entitlement, which occurs when you already have an active VA loan, limits your zero-down buying power to your remaining entitlement. Confirm your entitlement status before shopping so you know whether loan limit math affects your plan.

VA House Hacking in Dayton

House hacking with a VA loan is one of the most practical wealth-building strategies available to veterans. You buy a multifamily property, live in one unit, and rent the remaining units. The rent from the other units offsets your housing cost, sometimes dramatically.

Here is a simple example using a duplex in Dayton:

| Item | Monthly Amount |

| Total PITI payment | $2,200 |

| Rental income from second unit | $1,400 |

| Your effective housing cost | $800 |

Instead of paying $2,200 per month to live alone, your tenant covers most of your mortgage. You build equity, you reduce your housing expense, and you gain experience as a landlord.

The strategy works best when you go in with honest intent to live there, give the property time to stabilize during the first year, and build reserves rather than spending early cash flow. BGC serves veterans across the Dayton area including Beavercreek, Kettering, and Centerville and can discuss construction options for multifamily builds as well.

Pros and Cons of Using a VA Loan for Multifamily

Pros

- No down payment required in most cases

- No private mortgage insurance at any credit level

- Rental income from other units offsets your mortgage

- Build equity and cash flow at the same time

- More flexible credit requirements conventional loans

- Competitive interest rates backed by the VA

Cons

- Must live in one unit as your primary residence

- Lenders may require 3 to 6 months of cash reserves

- Self-sufficiency test can make triplex and fourplex deals harder

- Every unit must pass VA Minimum Property Requirements

- Landlord experience may be required to count rental income

- Fewer lenders handle multifamily VA files than single-family

VA vs FHA vs Conventional for Multifamily

| Feature | VA Loan | FHA Loan | Conventional Loan |

| Minimum down payment | 0% | 3.5% | 15% to 25% |

| Monthly mortgage insurance | None | Yes | Yes until 20% equity |

| Occupancy required | Yes | Yes | No for investors |

| Max units | 4 | 4 | 4 |

| Self-sufficiency test | Yes on 3 to 4 units | Yes on 3 to 4 units | No |

| Rental income counted | 75% of market rent | 75% of market rent | 75% with 2 year history |

| Typical credit floor | 580 to 620 | 580 | 680 and above |

For veterans who qualify, the VA loan wins on almost every line. No down payment and no mortgage insurance create a cash flow advantage from day one that FHA and conventional loans can’t match.

For veterans who qualify, the VA loan wins on almost every line. No down payment and no mortgage insurance create a cash flow advantage from day one that FHA and conventional loans cannot match. On a multifamily purchase, those differences add up to tens of thousands of dollars over the life of the loan.

Our home build and addition services are available for veterans who want to build a multifamily property from the ground up rather than buying an existing one, and our design-build remodeling and construction process walks through every step involved.

Best VA Lenders for Multifamily Properties

Not all VA lenders handle multifamily files. Many specialize in single-family purchases and treat multifamily as an exception. Here is what to look for:

- Direct experience closing VA multifamily loans in the past 12 months

- Clarity on reserve requirements upfront, not after you are under contract

- Willingness to explain their rental income calculation method

- Experience with the self-sufficiency test on three and four unit deals

- Manual underwriting capability for files that do not get a clean automated approval

Ask each lender specifically how many VA duplex, triplex, or fourplex loans they closed last year. That number tells you more than any marketing claim. Our guide to choosing the right lender for your VA construction loan in Dayton covers exactly what questions to ask.

Frequently Asked Questions

Can I buy a fourplex with a VA loan?

Yes. VA loans cover properties with up to four residential units. You must occupy one unit as your primary residence and every unit must meet VA Minimum Property Requirements.

Can I rent out all units eventually?

Yes, in most cases. Once you’ve established genuine occupancy, circumstances like PCS orders or other life changes can allow you to move out and rent all units. Moving out quickly after closing in a way that looks preplanned can create documentation questions.

Do I need landlord experience?

Many lenders require it or a documented property management plan before they will count rental income toward your qualification. Check your lender’s requirements early.

What is the VA self-sufficiency test?

It is a lender overlay applied on many three and four unit properties. The net rental income from non-owner units, after the 75% vacancy factor, must cover the full monthly mortgage payment. If it doesn’t, the lender may require more income or reserves.

Can rental income help me qualify?

Yes, but only at 75% of the appraiser’s market rent estimate. Most lenders also require reserves and may require landlord experience before counting it.

How do I start the process?

Confirm your VA eligibility and Certificate of Eligibility first. Then find a lender with real multifamily experience. Choose your property type and make sure every unit can pass a VA appraisal before you make an offer.

Are VA multifamily loans harder to get than single-family loans?

They’re more complex. More documentation is required, reserve requirements are higher, and fewer lenders handle them routinely. Working with an experienced lender and having your paperwork ready early makes the process manageable.

Ready to build or buy a multifamily property in Dayton using your VA benefit? Call BGC at 937-800-4409 or visit bgcnow.us to talk with our team today.