This is one of the most common questions veterans ask before applying for a home loan. The short answer is that the VA itself does not set a minimum credit score. Your lender does. Most lenders in Dayton require at least a 620, but some will work with scores as low as 580 or even lower with the right compensating factors.

If you are a veteran planning to build a home in Dayton, Builders Group Construction is a VA-approved builder who works alongside VA lenders and can connect you with financing contacts familiar with the local market. Visit bgcnow.us or call 937-800-4409 to get started.

Is There a Minimum Credit Score for VA Loans?

The Department of Veterans Affairs does not set a numeric credit score floor. VA guidelines require lenders to evaluate your overall creditworthiness, but they do not say your score must be 620 or any other number.

What you run into instead are lender overlays. These are internal risk thresholds that each lender sets on top of VA program rules. One lender might require 620. Another might accept 580. A specialist lender might go as low as 500 with strong compensating factors.

Every minimum score you see advertised by a VA lender is their overlay, not a VA rule. That distinction matters because shopping lenders is one of the most valuable things you can do if your score is on the lower end. For a broader look at how VA financing works from the start, our guide on how VA construction loans work is a good place to begin.

What Credit Score Do Most VA Lenders Require?

The 620 Standard

Most VA lenders in Dayton and across the country set their floor at 620. This is the point where automated underwriting systems most commonly return an approval on clean loan files. If your score is 620 or above, the majority of lenders will run your application without extra friction.

VA Loans With a 580 Credit Score

Some lenders will accept scores as low as 580. At this range, your full financial picture matters much more. Lenders look closely at your payment history, how much income you have left after expenses, and whether you have any savings in reserve. A 580 with zero late payments in the past year is a very different file from a 580 with recent missed payments.

Lenders like Guild Mortgage, Rocket Mortgage, and Freedom Mortgage publish minimums in the 550 to 580 range. Manual underwriting is often required at this level, and not every lender offers it. Our guide to the best VA construction loan lenders in Dayton covers which lenders are most flexible on credit requirements specifically for construction financing.

Can You Qualify With a 500 to 550 Credit Score?

Options become limited below 580, but they exist. Lenders like Carrington Mortgage publish minimums as low as 500. At this range, expect manual underwriting, strong residual income, clean recent payment history, and documented cash reserves. Approval is possible but requires finding the right lender and having a solid overall file.

Here is a quick snapshot of what major VA lenders publish:

| Lender | Published Minimum | Manual Underwriting |

| Veterans United | 620 | Yes |

| Navy Federal Credit Union | 620 | Varies |

| Rocket Mortgage | 580 | No |

| Freedom Mortgage | 550 | Sometimes |

| Guild Mortgage | 580 | Yes |

| Carrington Mortgage | 500 | Yes |

| USAA | 640 | Rarely |

Factors Lenders Consider Beyond Credit Score

Your credit score is just one part of your loan file. VA underwriting looks at the whole picture.

Debt-to-Income Ratio

Your debt-to-income ratio, or DTI, compares your monthly debt payments to your gross monthly income. The VA uses 41% as a general benchmark. Going above that does not automatically disqualify you, especially if your residual income is strong, but it does invite more scrutiny. For a full breakdown of how DTI affects your borrowing power, see our VA loan affordability guide.

Residual Income

This is the factor that makes VA underwriting unique. Residual income is the money left over each month after all major expenses are paid, including your mortgage, debts, taxes, and utilities. The VA sets regional thresholds based on family size. Exceeding that threshold by 20% or more is one of the strongest compensating factors you can have, especially when your credit score is marginal.

Certificate of Eligibility

Your Certificate of Eligibility, or COE, confirms to lenders that you have earned VA loan benefits. Without it, the loan cannot move forward. You can request it through the VA directly or ask your lender to pull it on your behalf. Veterans, active-duty service members, and eligible surviving spouses can all qualify for this benefit. Our VA entitlement explained guide covers how entitlement and eligibility work together.

Employment and Income Stability

Two or more years of consistent W-2 employment is what automated underwriting systems expect on clean files. Variable income like commissions, overtime, or self-employment requires additional documentation and can add friction when your score is already near the lender’s floor.

Cash reserves also matter. Even one to two months of mortgage payments sitting in a verifiable savings account can shift a borderline file in the right direction. Reserves are not required by the VA on most files, but lenders treat them as a risk offset when other factors are tight.

How Manual Underwriting Works for VA Loans

Manual underwriting happens when the automated underwriting system returns a Refer finding rather than an approval. This isn’t a denial. It means a human underwriter will review your file directly.

Files that go to manual underwriting often have lower scores, recent negative marks, higher DTI ratios, or income that is harder to document. The review requires stronger compensating factors and cleaner paperwork, but it’s a real path to approval.

Not all lenders offer manual underwriting for VA loans. Some process exclusively through automated systems and will decline any file that doesn’t get an automated approval. If your score is below 620, finding a lender that actively does manual underwriting is a critical step.

What helps in manual underwriting: 12 months of on-time payments with no lates, documented reserves, DTI below 41%, consistent employment history, and strong residual income above the regional threshold.

How Your Credit Score Affects Your Interest Rate

Your score does not just affect approval. It directly affects what rate you pay. Even small differences in interest rates add up significantly over the life of a loan.

Here is what that looks like in practice:

| Credit Score Range | Estimated Rate Impact | Monthly Difference on $350,000 Loan |

| 740 and above | Best available rate | Baseline |

| 680 to 739 | Small adjustment | Around $50 more |

| 620 to 679 | Moderate adjustment | Around $100 to $150 more |

| 580 to 619 | Significant adjustment | Around $175 or more |

The good news is that VA loans have no private mortgage insurance at any credit level. That saves hundreds per month compared to conventional loans, regardless of your score.

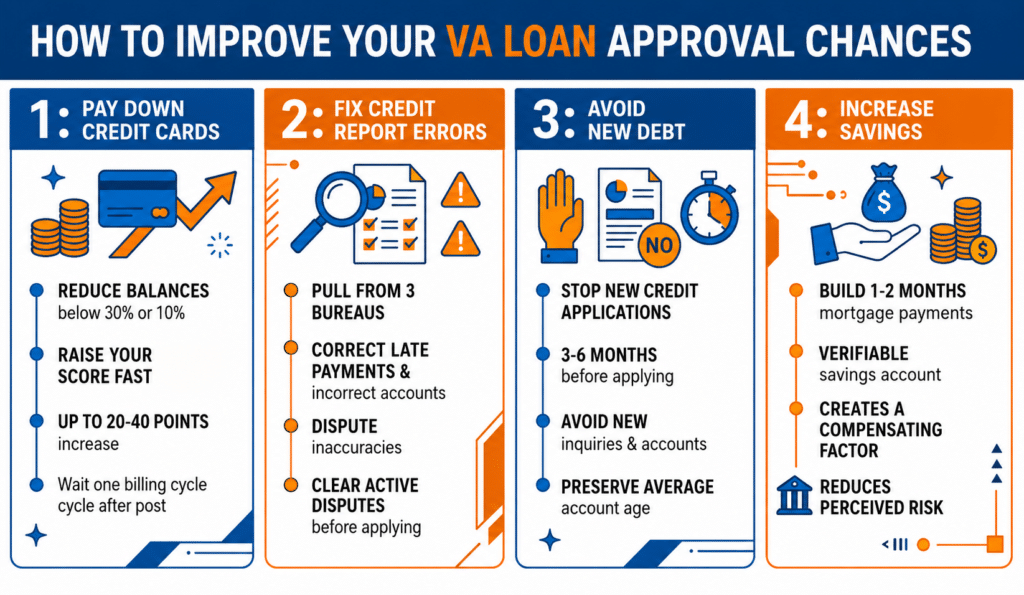

How to Improve Your VA Loan Approval Chances

If your score needs work before you apply, focus on moves that change the numbers quickly.

Pay Down Credit Cards

Reducing your credit card balances below 30% of each card’s limit is the fastest way to raise your score. Getting below 10% produces the maximum benefit. One billing cycle after the balance posts, your score updates. This single step can add 20 to 40 points on some files.

Fix Credit Report Errors

Pull your reports from all three bureaus and look for inaccurate late payments, wrong balances, or accounts that do not belong to you. Dispute anything incorrect. A removed collection or corrected late payment can add meaningful points. Clear any disputes before applying because an active dispute can slow down underwriting.

Avoid New Debt

Stop applying for any new credit three to six months before your VA loan application. Every new inquiry and every new account lowers your average account age and adds risk signals to your file.

Increase Savings

Build at least one to two months of mortgage payments in a verifiable savings account. This gives underwriters a concrete compensating factor and reduces perceived risk on files that are otherwise borderline.

VA Loan Credit Requirements vs FHA and Conventional

| Requirement | VA Loan | FHA Loan | Conventional Loan |

| Program minimum score | None | 500 to 580 | 620 |

| Typical lender overlay | 580 to 620 | 580 to 620 | 640 to 660 |

| Down payment | 0% in most cases | 3.5% to 10% | 3% to 5% |

| Mortgage insurance | None | Required | Required below 80% LTV |

| Manual underwriting | Yes | Limited | Rarely |

| Foreclosure waiting period | 2 years | 3 years | 7 years |

The VA loan is structurally the most flexible major loan program for veterans with lower credit scores. No down payment and no mortgage insurance make it the most affordable path to homeownership, offering excellent VA loan affordability even when your credit isn’t perfect.

For veterans in Dayton looking to build rather than buy, BGC handles VA construction projects across the area including Beavercreek, Kettering, and Centerville. Our home build and addition services are built around working with VA lenders from day one.

VA Construction Loan Timeline for Dayton Veterans

If your goal is to build a home using VA financing, here is the realistic timeline:

| Phase | Estimated Time |

| Credit preparation | 1 to 6 months if needed |

| Pre-approval and COE | 1 to 2 weeks |

| Builder approval | 2 to 4 weeks |

| Underwriting and appraisal | 2 to 3 weeks |

| Construction phase | 6 to 12 months |

| Final loan conversion | 1 to 2 weeks |

Getting your credit in order before you start the process is time well spent. A score increase from 590 to 625 can mean a lower rate, fewer lender restrictions, and a smoother approval. You can also review our guide on can you build a home with a VA loan to understand how each phase fits together once financing is in place. If you are ready to find the right builder, our guide on how to choose a builder for your VA construction loan in Dayton is the next step.

Frequently Asked Questions

Does the VA set a minimum credit score?

No. The VA requires lenders to evaluate creditworthiness but doesn’t publish a numeric floor. Every minimum you see is a lender overlay.

Can I get a VA loan with a 580 credit score?

Yes, with the right lender. Some lenders accept 580 with strong compensating factors like clean payment history, low DTI, and solid residual income. Manual underwriting is typically required at this range.

What disqualifies you from a VA loan?

Common disqualifiers include insufficient service history, a dishonorable discharge, income that does not meet residual income requirements, a score below the lender’s overlay, and active delinquencies on existing debts.

Do VA loans require good credit?

Not by VA standards. The program has no official credit floor. Lender overlays create practical minimums, but the program is designed to be more flexible than conventional financing.

Can I buy a house with a 550 credit score using a VA loan?

Some lenders will work with a 550 score. Expect manual underwriting, strong residual income, clean recent payment history, and documented reserves. Options are limited but available.

Is manual underwriting harder to get approved through?

Paying down revolving balances can add points within one billing cycle. Removing errors through disputes takes 30 to 45 days. Recovering from a recent late payment typically requires 6 to 12 months of clean history.

How long does it take to raise my score?

Paying down revolving balances can add points within one billing cycle. Removing errors through disputes takes 30 to 45 days. Recovering from a recent late payment typically requires 6 to 12 months of clean history.

Ready to use your VA benefit to build in Dayton? Call BGC at 937-800-4409 or visit bgcnow.us to connect with our team and get started today.