Yes, you can. Many veterans assume VA loans only work for buying existing homes. That’s not true. If you’re eligible, you can use your VA benefit to build a brand new custom home in Dayton with no down payment and no private mortgage insurance.

This is called a VA construction loan. It covers the cost of building your home and then converts into a permanent mortgage when the build is complete. Builders Group Construction is a VA-approved builder in Dayton that works with veterans through every step of this process, from lot selection to final walkthrough. Visit bgcnow.us to learn more or schedule a free consultation.

Can You Build a Home with a VA Loan?

A VA construction loan is different from a standard VA purchase loan. A standard VA loan helps you buy a home that already exists. A construction loan finances the actual build, from breaking ground to handing over the keys.

The Department of Veterans Affairs guarantees a portion of the loan. This reduces risk for lenders and allows them to offer better terms to veterans. The process is more involved than buying an existing home, but the benefits are significant. The no down payment option alone sets VA construction financing apart from most conventional alternatives.

The home must be your primary residence. Investment properties and vacation homes do not qualify.

How Does a VA Construction Loan Work in Dayton?

Step 1: Obtain Your Certificate of Eligibility

Your Certificate of Eligibility, or COE, confirms to lenders that you have earned VA loan benefits through your military service. You can request it directly through the VA or ask your lender to pull it on your behalf. Most lenders can do this quickly through an online system.

Veterans, active-duty service members, and eligible surviving spouses can all qualify. Service length and discharge status affect eligibility, so check your specific situation with a VA-approved lender early in the process.

Step 2: Find a VA Construction Loan Lender in Dayton

This step trips up a lot of veterans. VA construction loans are not offered by every lender. The product requires more underwriting work and carries more risk than a standard purchase loan, so fewer banks and credit unions offer it.

When comparing lenders, ask how many VA construction loans they have closed in the last 12 months. Ask if they offer one-time close financing. Ask who handles the draw inspections. These questions quickly separate experienced lenders from those who are figuring it out as they go.

Step 3: Choose a VA-Approved Builder

This is one of the most important steps in the whole process. The VA requires that your builder be registered and approved before the loan can move forward. A builder who isn’t VA-registered can’t be used on your project, period.

To be VA-approved, a builder must be licensed in the state where they are building, fully insured, and registered directly with the VA. Builders Group Construction meets all of these requirements. As part of our home build and addition services, we work directly with your lender and handle the builder registration side so you do not have to chase paperwork on your own.

Common reasons builders get disqualified include expired licenses, insufficient insurance coverage, and failure to register with the VA before construction begins. Choosing an already-approved builder from the start saves weeks of time.

Step 4: Secure Construction Plans and Appraisal

Once your builder is confirmed, your lender will order a subject-to-completion appraisal. An appraiser reviews your blueprints and construction specs and estimates what the finished home will be worth. The loan amount is based on that estimate, not the cost of building.

Your plans must also show that the home will meet VA Minimum Property Requirements. These cover things like structural soundness, safe electrical systems, and proper insulation. BGC designs homes to meet these standards from day one, which prevents costly redesigns later.

Step 5: The Construction Draw Schedule

Rather than releasing the full loan amount upfront, the lender releases funds in stages throughout the build. These are called draws. Each draw is released after a completed phase passes inspection.

Here is a typical draw schedule:

| Construction Phase | When Funds Are Released |

| Foundation poured and complete | Draw 1 |

| Framing complete | Draw 2 |

| Rough plumbing, electrical, HVAC done | Draw 3 |

| Drywall, insulation, interior work | Draw 4 |

| Final completion and punch list | Draw 5 |

An inspector visits the site before each draw is approved. This protects both you and the lender and ensures the builder completes each phase properly before receiving payment. Funds are held in a construction escrow account between draws.

Step 6: Loan Conversion to Permanent Mortgage

When the home is fully built and passes final inspection, your VA construction loan converts to a permanent VA mortgage. This is the one-time close advantage. You applied once, closed once, and now simply begin making regular monthly mortgage payments.

There is no second closing, no second round of closing costs, and no scramble to lock a new rate after construction ends..

What Types of Homes Can You Build with a VA Loan?

Custom Homes

This is the most common use. Veterans work with a VA-approved builder to design and build a fully custom home on a chosen lot. Floor plan, layout, finishes, and features are all chosen by the homeowner. Our design-build remodeling and construction process is built around this kind of project.

Modular Homes

Modular homes are built in sections at a factory and assembled on site. They can qualify for VA financing if they meet VA Minimum Property Requirements and are placed on a permanent foundation. Not all lenders finance modular construction, so ask upfront.

Manufactured Homes

VA loans can cover manufactured homes in certain situations. The home must be on a permanent foundation and meet HUD standards. Lender availability is more limited for this property type, and the terms may differ from standard construction financing.

Stick-Built Homes

Stick-built refers to homes constructed on-site using traditional framing methods. This is the most widely accepted home type for VA construction financing and the easiest to get approved.

Can You Buy Land and Build with a VA Loan?

In many cases, yes. Some VA construction loan programs allow you to roll the cost of purchasing land into the same loan as the construction. This means you’re financing the land, the build, and the permanent mortgage all together.

If you already own the land, its value may be counted toward your VA entitlement, which can reduce your overall loan amount. Not every lender offers combined land and construction financing, so make sure to ask about it before you choose your lender. The land must be intended for your primary residence, and there may be restrictions on lot size depending on the lender.

One-Time Close vs Two-Time Close VA Construction Loans

| Feature | One-Time Close | Two-Time Close |

| Number of closings | One | Two |

| Closing costs | Lower | Higher |

| Rate lock | Locked before construction | Locked after construction |

| Process complexity | Simpler | More steps involved |

| Risk of rate increase | Lower | Higher |

The one-time close option is the better choice for most veterans. You lock your interest rate before construction begins, pay closing costs only once, and avoid the uncertainty of qualifying again after the build is done. BGC works with lenders who offer one-time close VA construction loans specifically.

VA Construction Loan Requirements

Here is what you need to qualify:

- Veteran, active-duty service member, or eligible surviving spouse status

- Valid Certificate of Eligibility

- Credit score of at least 620 (some lenders may vary)

- Debt-to-income ratio within lender guidelines

- Sufficient residual income after monthly expenses

- VA-approved and registered builder

- Approved blueprints and construction specifications

- Subject-to-completion appraisal

- Home intended as primary residence

Residual income is one of the most important factors the VA looks at. It’s the money you have left over each month after paying all debts and housing costs. The VA construction loan requirement amount varies by family size and region.

Challenges with VA Construction Loans and How to Handle Them

VA construction loans are more complex than standard VA purchase loans. Understanding the common challenges ahead of time puts you in a much stronger position.

Fewer lenders offer this product. The underwriting is more involved and construction projects carry more risk. Many banks simply avoid this loan type. Search specifically for lenders with a track record of closing VA construction loans, not just VA purchase loans.

Builder approval adds a step. If your builder is not already VA-registered, you will lose time getting them approved or need to find a different builder. Choose a builder who is already registered before you start the loan process.

Construction timelines and cost overruns concern lenders. Delays and incomplete builds create risk that does not exist when buying a finished home. Work with a builder who has documented experience on VA construction projects specifically.

Coming in prepared with your COE ready, a registered builder selected, and your credit in good shape removes most of the friction veterans run into. You can learn more about how we handle this through our home construction process.

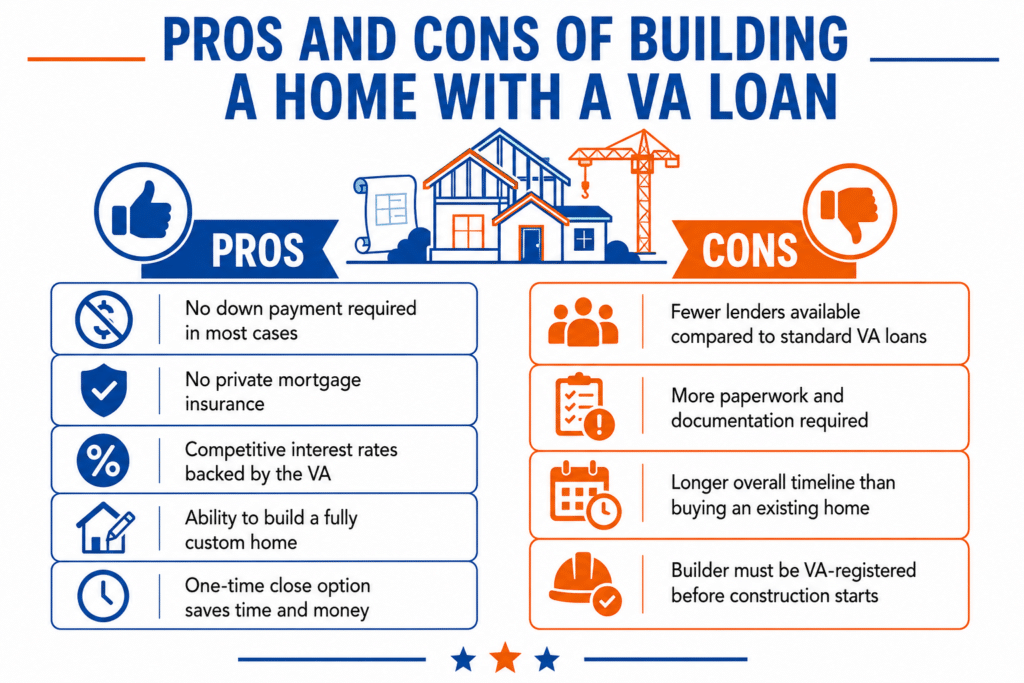

Pros and Cons of Building a Home with a VA Loan

Pros

- No down payment required in most cases

- No private mortgage insurance

- Competitive interest rates backed by the VA

- Ability to build a fully custom home

- One-time close option saves time and money

Cons

- Fewer lenders available compared to standard VA loans

- More paperwork and documentation required

- Longer overall timeline than buying an existing home

- Builder must be VA-registered before construction starts

VA Construction Loan Costs and Fees

Here is what to budget for beyond the construction costs themselves:

- VA funding fee: typically 1.25% to 3.3% of the loan amount depending on service history and down payment

- Appraisal fee: usually between $500 and $1,500 for a subject-to-completion appraisal

- Draw inspection fees: charged each time an inspector visits the site before a draw is released

- Interest reserve account: covers the interest that accrues during the construction phase before the loan converts

- Builder deposit: varies by builder and project scope

- Title and closing costs: standard for any mortgage closing

The interest reserve account is something many veterans overlook. During construction, you’re not making principal payments yet, but interest is still accruing. This account covers that cost so you’re not paying out of pocket while the home is being built.

According to Veterans United Home Loans, total costs on VA construction loans are still typically lower than conventional construction financing when you factor in the savings from no down payment and no PMI.

In Dayton, total closing costs on a VA construction loan typically fall between 2% and 5% of the loan amount. Your lender should provide a full loan estimate before you commit to anything.

VA Construction Loan Timeline

| Phase | Estimated Time |

| Pre-approval and COE verification | 1 to 2 weeks |

| Builder approval and plan finalization | 2 to 4 weeks |

| Underwriting and appraisal | 2 to 3 weeks |

| Construction phase | 6 to 12 months |

| Final inspection and loan conversion | 1 to 2 weeks |

For a typical custom home in Dayton, plan for the full process to take between 9 and 15 months from your first lender conversation to move-in day. Homes with more complex designs or custom finishes may take longer. BGC serves veterans building in cities like Kettering, Beavercreek, and Tipp City and follows this same general timeline across all locations.

Common Reasons VA Construction Loans Get Denied

Knowing what causes denials helps you avoid them:

- Builder is not VA-registered at the time of application

- Credit score falls below lender minimums

- Construction plans are incomplete or do not meet VA property requirements

- The appraisal comes in lower than the expected construction cost

- Income does not meet residual income requirements

- The property type does not meet VA standards

- Debt-to-income ratio is too high

Most of these issues can be addressed before you apply. Get your builder approved first. Work on your credit at least six months before applying. Prepare detailed, complete construction plans that your builder and lender can review together before submission.

Frequently Asked Questions

Can you build a custom home with a VA loan?

Yes. VA construction loans are specifically designed for building custom homes. You choose the lot, the floor plan, and the finishes

Can a VA loan cover land and construction together?

In many cases, yes. Some lenders allow you to finance the land purchase and the construction costs in one loan. Confirm this with your lender early in the process.

Do VA construction loans require a down payment?

In most cases, no. That is one of the biggest advantages of using your VA benefit to build rather than using a conventional construction loan

What credit score is needed for a VA construction loan?

Most VA construction lenders want a minimum credit score of 620. Some lenders may accept lower scores depending on other factors in your application.

Can modular homes qualify for VA financing?

Yes, in many cases. The home must be placed on a permanent foundation and meet VA Minimum Property Requirements. Lender availability for modular construction is more limited than for stick-built homes.

How do construction draws work?

Funds are released in stages as each phase of construction is completed and inspected. A draw inspector visits the site before each payment is approved.

Why are VA construction loans difficult to get?

Fewer lenders offer them, underwriting is more complex, and builders must be VA-registered. Working with an experienced builder and lender from the start makes the process much smoother.

What is a one-time close VA loan?

It is a loan where you close once before construction begins. The construction financing and the permanent mortgage are combined into a single loan with one set of closing costs.

How long does it take to build a home with a VA loan?

From pre-approval to move-in, most veterans should plan for 9 to 15 months total.

Can I use my own builder?

Only if your builder is VA-registered. If they are not already approved, they will need to go through the registration process before construction can begin.

Ready to build your home in Dayton? Call BGC at 937-800-4409 or visit bgcnow.us to schedule your free consultation today.