Finding a VA construction loan lender in Dayton is harder than finding a standard VA mortgage lender. Most banks offer VA purchase loans. Far fewer offer VA construction financing. The underwriting is more complex, the timelines are longer, and the builder approval process adds steps that most lenders would rather avoid.

That is why choosing the right lender from the start matters so much. The wrong lender can slow down your builder approval, mismanage your draw schedule, or leave you without clear answers during a 10-month build. The right lender makes the whole process feel manageable.

If you are a veteran ready to build in Dayton, Builders Group Construction is a VA-approved builder that already works with VA construction lenders and can help you move faster from pre-approval to breaking ground. Visit bgcnow.us or call 937-800-4409 to get started.

What Is a VA Construction Loan?

A VA construction loan finances the actual build of a home rather than the purchase of an existing one. The Department of Veterans Affairs guarantees a portion of the loan, which reduces risk for lenders and allows them to offer better terms to veterans.

Once construction is complete and the home passes final inspection, the loan converts to a permanent VA mortgage. With a one-time close structure, this happens without a second closing or a second set of costs.

The home must be your primary residence. Investment properties and vacation homes do not qualify.

Why Choosing the Right VA Construction Loan Lender Matters

VA construction loans are not a standard product. Most loan officers handle them a handful of times per year at best. That lack of experience creates real problems for borrowers.

An inexperienced lender may not know how to process builder approvals efficiently. They may not understand draw schedule management, which causes payment delays to your builder. They may not coordinate well with VA appraisers who handle subject-to-completion appraisals. Any one of these issues can add weeks or months to your timeline.

The right lender has done this before. They know the construction escrow process, they communicate proactively, and they keep your project moving even when small problems come up. For a build that takes 6 to 12 months, that consistency matters more than almost anything else.

Best VA Construction Loan Lenders in Dayton

The lenders below are evaluated based on VA construction experience, one-time close availability, builder approval speed, customer service, and overall transparency on fees. This is not a paid list. These are lenders worth researching based on their track record with VA construction financing.

Veterans United Home Loans

Veterans United is one of the largest VA mortgage lenders in the country. They focus almost entirely on veteran financing, which means their loan officers tend to know VA guidelines well. Their customer support is strong and they offer educational resources that help first-time VA borrowers understand the process.

For construction loans specifically, Veterans United has experience with one-time close financing. Their main strength is on the borrower support side. Veterans who want clear communication and a dedicated loan team will find them easy to work with.

Best for: First-time VA borrowers who want strong support through a complex process.

VA Nationwide

VA Nationwide is a lender that focuses specifically on VA construction financing. That specialization matters. They handle one-time close construction loans regularly and have systems built around builder coordination and draw schedule management.

Because construction loans are their core focus rather than a side product, they tend to move faster on builder approvals and understand the inspection process well. If your priority is finding someone who does this every day, VA Nationwide is worth a serious look.

Best for: Veterans who want a lender with deep VA construction experience and fast builder approval.

Rocket Mortgage

Rocket Mortgage is known for its digital-first experience and fast online application process. For veterans who are comfortable managing their loan online and want a smooth digital interface, Rocket offers a strong platform.

Their VA construction loan availability is more limited than specialized lenders. They’re better known for standard VA purchase and refinance loans than for construction-to-permanent financing. If you go this route, confirm upfront that they can handle your specific construction loan needs in Ohio.

Best for: Tech-comfortable borrowers who prioritize a strong online experience.

Guild Mortgage

Guild Mortgage has a reputation for being flexible with builders and accommodating loan structures. They work with a wide range of builders and have experience processing VA construction loans in multiple states including Ohio.

Their regional teams tend to have good knowledge of local markets, which helps with appraisal coordination and permit-related timelines. They’re a solid choice for veterans who have already chosen a builder and want a lender that will work well with that builder’s schedule.

Best for: Veterans with an existing builder relationship who need a lender that coordinates well with contractors.

Pennymac

Pennymac is a large national lender with competitive rates and a strong online servicing platform. They offer VA loans broadly and have reasonable fees compared to some larger banks.

Their VA construction loan availability is more limited, and they are not as specialized in construction-to-permanent financing as others on this list. For veterans who qualify well and are primarily focused on rate competitiveness, they are worth comparing.

Best for: Rate-focused borrowers who meet strong qualification criteria.

Comparison Table

| Lender | One-Time Close | Builder Approval Support | Online Experience | Best For |

| Veterans United | Yes | Strong | Moderate | First-time VA borrowers |

| VA Nationwide | Yes | Excellent | Moderate | Construction specialists |

| Rocket Mortgage | Limited | Moderate | Excellent | Digital-first borrowers |

| Guild Mortgage | Yes | Strong | Moderate | Builder flexibility |

| Pennymac | Limited | Moderate | Strong | Competitive rates |

How to Choose the Right VA Construction Loan Lender

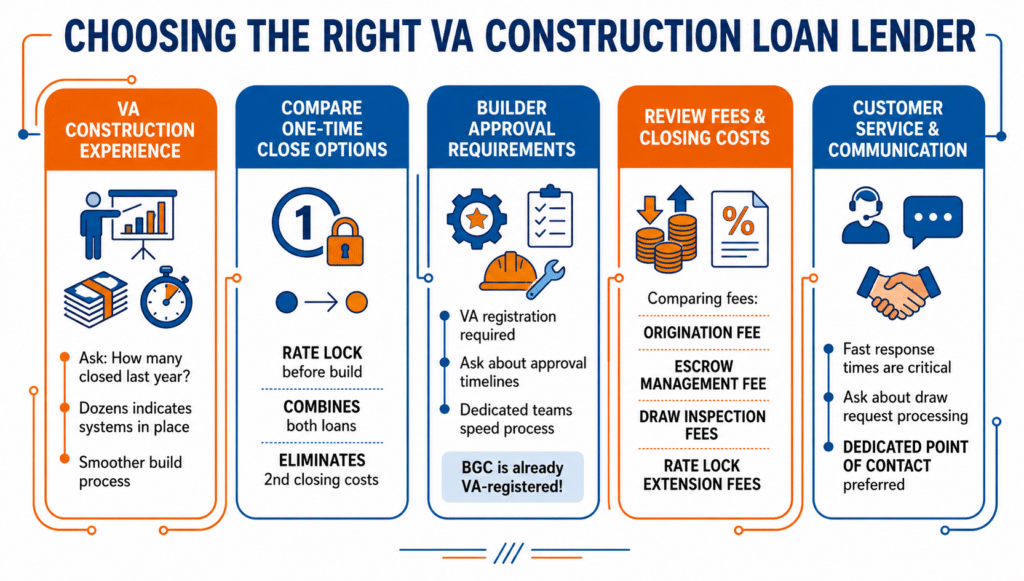

Look for VA Construction Experience

Ask any lender directly: how many VA construction loans did you close last year? A lender who closes five or fewer is still learning. A lender who closes dozens has systems in place for draw management, builder coordination, and appraisal scheduling. That experience directly affects how smooth your build goes.

Construction underwriting is more involved than a standard purchase loan. You want a loan officer who has seen common problems before and knows how to handle them without delays.

Compare One-Time Close Loan Options

Not every lender offers a true one-time close VA construction loan. Some require two separate closings, which means two sets of closing costs and a second round of qualification after your build is done.

The one-time close option locks your rate before construction begins, combines both loans into one, and eliminates the second closing entirely. For most veterans, this is the better structure. Confirm that any lender you consider offers it before you go further in the process. You can learn more about how BGC approaches the overall construction process and how lender coordination fits into each phase.

Ask About Builder Approval Requirements

Builder approval is one of the biggest bottlenecks in VA construction financing. The VA requires that your builder be registered and approved. Different lenders handle this process at different speeds.

Some lenders have internal teams dedicated to builder approval. Others treat it as an afterthought. Ask specifically how long builder approval takes, what documents they need from your builder, and whether they have worked with VA-registered builders in the Dayton area before.

BGC is already VA-registered, which removes this step entirely and speeds up your overall timeline. Our home build and addition services are set up to work directly with VA lenders from day one.

Review Fees and Closing Costs

VA construction loans involve more fees than standard purchase loans. Here is what to compare across lenders:

- Origination fee

- Construction escrow management fee

- Draw inspection fees per visit

- Rate lock extension fees if your build runs long

- Appraisal fees for subject-to-completion review

Ask each lender for a full fee breakdown before you commit. Some lenders are transparent about these costs upfront. Others bury them. The National Association of Mortgage Brokers recommends comparing loan estimates side by side to catch fee differences that are not obvious at first glance.

Evaluate Customer Service and Communication

During a 6 to 12 month build, you will have many questions. Draw approvals, inspection scheduling, rate lock extensions, and builder payments all require lender involvement. A lender who is slow to respond or unclear in their communication creates stress throughout the entire build.

Ask each lender who your primary point of contact will be. Ask how draw requests are submitted and how quickly they are processed. Ask if they assign a dedicated loan officer for the life of the construction project or if your file gets passed around.

One-Time Close vs Two-Time Close VA Construction Loans

| Feature | One-Time Close | Two-Time Close |

| Number of closings | One | Two |

| Closing costs | Lower | Higher |

| Rate lock | Locked before construction | Locked after construction |

| Process complexity | Simpler | More steps involved |

| Risk of rate increase | Lower | Higher |

For most veterans building in Dayton, the one-time close structure is the right choice. You avoid paying closing costs twice, you lock your rate early, and you don’t have to re-qualify for financing after your home is built. If your financial situation could change during a long build, the one-time close protects you from that risk.

Common Problems Borrowers Face with VA Construction Lenders

Builder approval delays. If your lender does not have a clear process for VA builder registration, expect delays. This can hold up your entire project start date. Choose a builder who is already approved to avoid this entirely.

Draw schedule confusion. Some borrowers do not fully understand that funds are released in stages, not all at once. When a draw is delayed because paperwork is incomplete or an inspection has not been scheduled, it can slow the builder down and cause friction. Ask your lender to walk you through the exact draw process before you close.

Limited communication during the build. Once the loan closes, some lenders go quiet until the final conversion. That leaves borrowers without clear answers when problems come up. Ask about communication frequency upfront.

Unexpected rate lock extension fees. If your build runs longer than expected, your rate lock may expire. Extending it costs money. Ask your lender what their rate lock extension policy is and what it costs per extension period.

Fee surprises at closing. Construction loans involve more fees than standard mortgages. Get a complete fee list in writing before you choose a lender.

Questions to Ask Before Choosing a VA Construction Loan Lender

These questions will quickly reveal how experienced a lender actually is:

- How many VA construction loans have you closed in the past 12 months?

- Do you offer one-time close VA construction loans?

- How long does your builder approval process take?

- What are your construction escrow management fees?

- Do you handle draw inspections internally or through a third party?

- Can I use a builder who is already VA-registered?

- What is your minimum credit score requirement?

- What happens if my build runs over the rate lock period?

- Who is my dedicated point of contact during the construction phase?

A lender who answers these questions clearly and confidently has done this before. A lender who stumbles or gives vague answers probably has not.

VA Construction Loan Requirements

Here is a quick checklist of what you need to qualify:

- Veteran, active-duty service member, or eligible surviving spouse status

- Valid Certificate of Eligibility

- Credit score of at least 620 (varies by lender)

- Debt-to-income ratio within lender guidelines

- Sufficient residual income after all monthly expenses

- VA-approved and registered builder

- Approved blueprints and construction plans

- Subject-to-completion appraisal completed

- Home must be your primary residence

Residual income standards vary by family size and geographic region, and meeting this requirement is one of the most important factors in VA loan approval.

Realistic VA Construction Loan Timeline

| Phase | Estimated Time |

| Pre-approval and COE verification | 1 to 2 weeks |

| Builder approval and plan finalization | 2 to 4 weeks |

| Underwriting and appraisal | 2 to 3 weeks |

| Construction phase | 6 to 12 months |

| Final inspection and loan conversion | 1 to 2 weeks |

For a veteran building a custom home in Dayton, the realistic total timeline is 9 to 15 months from first lender contact to move-in day. Working with a VA-registered builder removes the builder approval wait time entirely and gets construction started faster.

BGC serves veterans across the Dayton area including Beavercreek, Kettering, and Centerville. Each project follows this same general timeline with regular progress updates throughout the build.

Best Local VA Construction Loan Options in Dayton

National lenders have scale, but local lenders and regional mortgage companies sometimes offer advantages that matter for a Dayton build specifically.

A local lender knows the Dayton permit office timelines, understands the regional appraisal market, and may already have relationships with local VA appraisers. That familiarity can speed up inspections and reduce appraisal surprises.

When comparing local versus national lenders, weigh the following. National lenders often have stronger technology and more loan officer availability. Local lenders often have faster local decision-making and better knowledge of your specific market. The best choice depends on your priorities, but do not overlook regional mortgage companies when you are shopping.

BGC works with both national and local lenders and can connect you with VA construction financing contacts in the Dayton area who already understand our build process and timelines. Our design-build services are structured to make that lender coordination as smooth as possible.

Frequently Asked Questions

Which lender is best for VA construction loans?

Veterans United and VA Nationwide are strong options for most veterans due to their focus on VA financing and one-time close loan availability. The best lender depends on your priorities around service, fees, and builder flexibility.

What is a one-time close VA construction loan?

It’s a loan structure where you close once before construction begins. The construction financing and permanent mortgage are combined into a single loan, saving you from a second closing and second set of costs.

Why are VA construction loans hard to find?

Most lenders prefer simpler loan products. VA construction loans require more underwriting, builder coordination, and draw management than standard purchase loans, so fewer lenders offer them.

Can I use my own builder?

Only if your builder is VA-registered. If they are not already approved, they must complete the registration process before construction can begin.

What credit score is needed?

Most VA construction lenders require at least 620. Some may accept lower scores depending on the full picture of your application.

How long does approval take?

Pre-approval takes 1 to 2 weeks. Builder approval adds another 2 to 4 weeks. Working with a VA-registered builder like BGC removes that second wait entirely.

Which lenders approve builders fastest?

Lenders who specialize in VA construction financing, like VA Nationwide, tend to have faster builder approval processes because they handle it regularly.

Are VA construction loans worth it?

For veterans who want a custom home, yes. No down payment and no PMI make it one of the most affordable ways to build, even with the added complexity.

What fees should I compare between lenders?

Compare origination fees, construction escrow fees, draw inspection costs, appraisal fees, and rate lock extension policies

Can VA construction loans finance land and construction together?

In many cases, yes. Confirm with your lender upfront whether they offer combined land and construction financing in Ohio.

Ready to start your build in Dayton? Call BGC at 937-800-4409 or visit bgcnow.us to connect with our team and get your VA construction project moving today.