If you are a veteran looking to buy a home, you have probably heard the term “VA entitlement.” Most people hear it and assume it means the amount they can borrow. That is not correct. VA entitlement is the amount the Department of Veterans Affairs guarantees to your lender if you stop making payments. It is a promise from the VA to back part of your loan.

This guarantee is what makes VA loans so useful. Lenders take on less risk, so they offer better terms. That often means no down payment and no private mortgage insurance. If you are working with a VA-approved builder in Dayton, understanding entitlement helps you plan your build with confidence.

At Builders Group Construction, we work with veterans on home builds, additions, and remodels. We understand how VA financing connects to the construction process, and we want to help you go in prepared.

What Is VA Loan Entitlement?

The VA does not give you the money to buy a home. Instead, it tells your lender: if this veteran defaults, we will cover part of the loss. That promise is your entitlement.

Because the VA backs a portion of the loan, lenders feel safe offering zero down payment options. No private mortgage insurance is required either. This is one reason VA loans are among the best mortgage options available to veterans and active service members.

Your entitlement amount is listed on your Certificate of Eligibility, also called a COE. Your lender can pull this document to see how much entitlement you currently have available. For a full breakdown of how the COE connects to your loan approval, see our guide on what credit score do you need for a VA loan.

VA Entitlement Is NOT a Loan Limit

This is the biggest misconception. VA entitlement does not cap what you can borrow. It only determines how much the VA will guarantee.

If you have full entitlement, the VA removed its official loan limits for you after 2019. You can borrow what your income and credit support. The VA is not capping your purchase price.

Loan limits still matter in certain situations, which we will cover below. But do not confuse entitlement with a borrowing ceiling. For a full picture of how much you can borrow based on your income and debts, our VA loan affordability guide walks through every factor lenders consider.

Basic Entitlement vs Bonus Entitlement

What Is Basic Entitlement?

Basic entitlement is $36,000. You will see this number on your COE. Historically, this figure allowed veterans to buy homes valued up to $144,000 without a down payment. The VA guaranteed 25% of that amount, which was $36,000.

Home prices are much higher today. That is where bonus entitlement comes in.

What Is Bonus (Second-Tier) Entitlement?

Bonus entitlement, also called second-tier entitlement, extends your coverage beyond the basic amount. It allows you to buy higher-priced homes and still get VA loan benefits. The VA will guarantee 25% of your loan amount under this tier, as long as you have full entitlement.

Why the $36,000 Number Confuses Veterans

Many veterans see $36,000 on their COE and think that’s their limit. It’s not. That is just the basic portion. If you have full entitlement, your total guarantee is 25% of your loan, no matter how large the loan is.

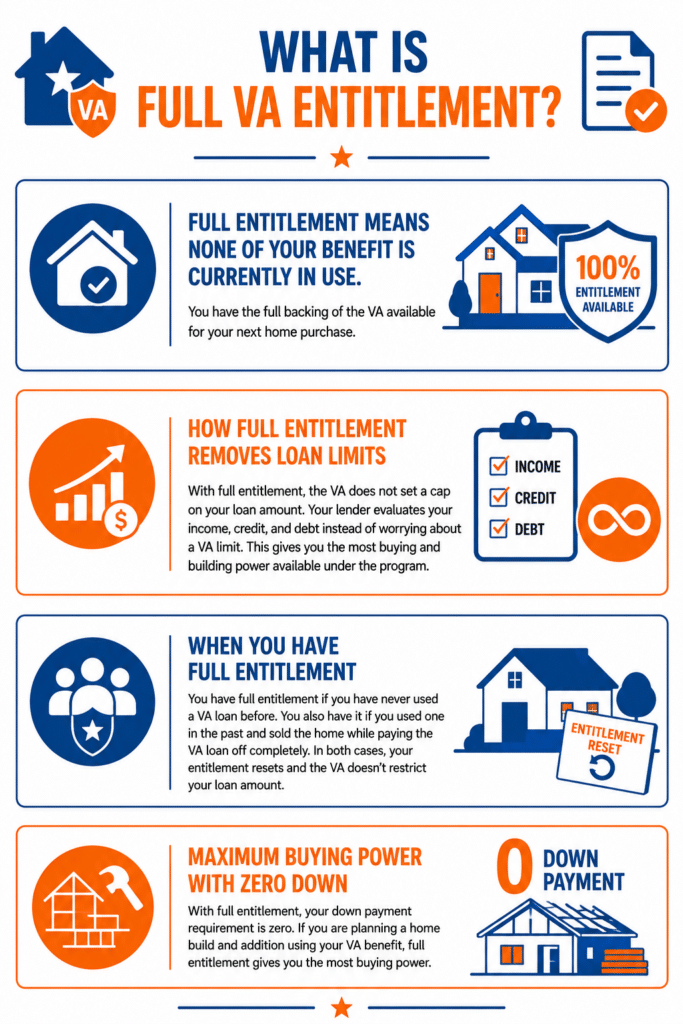

What Is Full VA Entitlement?

Full entitlement means none of your benefit is currently in use. You have the full backing of the VA available for your next home purchase.

How Full Entitlement Removes Loan Limits

With full entitlement, the VA does not set a cap on your loan amount. Your lender evaluates your income, credit, and debt instead of worrying about a VA limit. This gives you the most buying and building power available under the program.

When You Have Full Entitlement

You have full entitlement if you have never used a VA loan before. You also have it if you used one in the past and sold the home while paying the VA loan off completely. In both cases, your entitlement resets and the VA doesn’t restrict your loan amount.

With full entitlement, your down payment requirement is zero. If you are planning a home build and addition using your VA benefit, full entitlement gives you the most buying power.

What Is Remaining or Partial Entitlement?

Partial entitlement happens when part of your benefit is still tied to an active VA loan. You used your entitlement on a home and still own it. That portion isn’t available for a new purchase.

How Existing VA Loans Affect Entitlement

Say you bought a home for $400,000 using a VA loan. You made no down payment. That means the VA guaranteed 25% of $400,000, which is $100,000. That $100,000 is now committed to your current home.

If you want to buy another home before selling the first one, you only have the remaining portion of your entitlement to work with.

Buying Another Home With Remaining Entitlement

You can still buy another home with partial entitlement. But your lender may require a down payment to cover the gap between your available entitlement and the 25% guarantee they need.

For example, if your county loan limit is $600,000, the VA would normally guarantee $150,000 (25%). Since $100,000 is already used, you only have $50,000 left. For an $800,000 purchase, your lender might require a down payment of up to $150,000.

Veterans using remaining entitlement through a cash-out refinance to fund a kitchen remodeling project may also want to review how partial entitlement affects their available equity before starting.

How to Calculate Your VA Entitlement

Simple Formula Examples

The VA guarantees 25% of the loan. To see what you need:

- Find your county loan limit from the FHFA website

- Multiply it by 25% to get the max guaranty for your area

- Subtract any entitlement already in use

- The result is your remaining entitlement

County Loan Limit Examples

For most counties in Ohio, the 2026 conforming loan limit is $806,500. That means the VA would guarantee up to $201,625. If you have used $100,000 of that, you have $101,625 remaining.

High-Cost Area Calculations

High-cost counties can have limits up to $1,209,750. Veterans buying in those areas can access a larger guarantee. Check VA.gov for the most current county limits in your area.

How to Restore Your VA Entitlement

Selling the Home

If you sell your home and pay off the VA loan in full, your entitlement is restored. You can use your full benefit again for a new purchase.

Paying Off the VA Loan

Paying off the balance through a refinance or lump sum also restores entitlement. You must close out the VA loan entirely, not just reduce the balance.

One-Time Restoration Rules

There is a one-time exception. If you paid off your VA loan but still own the home, you may be able to restore your entitlement once to buy a new primary residence. This option exists to let veterans move without losing their benefit, not to finance rental properties.

Veterans who have gone through a design build remodel often ask about this option when upgrading to a larger home.

How to Check Your VA Entitlement

Reading Your COE

Your lender can pull your Certificate of Eligibility directly through the VA system. It shows your current entitlement status and any existing commitments.

Understanding Entitlement Codes

Your COE includes an entitlement code. This code tells lenders why you qualify and what type of service made you eligible. It doesn’t affect your entitlement amount, but lenders use it to verify your status.

Veterans considering a bathroom remodeling project funded through a VA cash-out loan should check their COE first. Knowing your available equity and entitlement before starting saves time and keeps your project on track.

VA Entitlement and Construction Loans

If you are planning to build rather than buy, entitlement works the same way. The VA still guarantees 25% of the loan, and full entitlement means no VA-imposed cap on your build cost. Working with a VA-approved builder in Dayton ensures your construction project is set up correctly from the financing side from day one.

For a full walkthrough of how construction financing connects to entitlement, our guide on can you build a home with a VA loan covers every step. If you are comparing lenders for your build, our best VA construction loan lenders in Dayton guide covers what to look for. BGC serves veterans across the Dayton area including Beavercreek, Kettering, Centerville, Tipp City, and Vandalia.

Frequently Asked Questions

How much VA entitlement do I have left?

Pull your COE through your lender. It shows your current entitlement amount. Your lender can also calculate the remaining amount based on any active VA loans.

Can I use my VA loan twice?

Yes. VA loans can be used more than once. Full restoration is available after selling and paying off a prior VA loan. Partial entitlement lets you use the benefit again even before the first loan is paid.

Does entitlement limit home price?

No. For veterans with full entitlement, there’s no VA-set price limit. Your lender approves you based on income, debt, and credit.

What is bonus entitlement?

Bonus entitlement is the additional guarantee amount beyond the basic $36,000. It covers higher-priced homes and gives veterans access to VA benefits on larger purchases.

How do I restore entitlement?

Sell the home and repay the loan, or refinance into a non-VA loan and apply for restoration using VA Form 26-1880. Include proof of payoff with your request.

Final Thoughts

VA entitlement is simply a financial guarantee from the VA to your lender. It’s not your loan limit. It’s not a cap on your home price. It is the backing that makes VA loans accessible and affordable for those who served.

Knowing whether you have full or partial entitlement helps you plan your next purchase with clarity. If you’re a veteran in the Dayton area thinking about building, buying, or remodeling, knowing your entitlement status is a smart first step.

For questions about VA-approved construction and remodeling in Ohio, contact BGC at 937-800-4409 or email info@bgcnow.us. Our office at 8450 E. Westbrook Road, Brookville is open Monday through Friday, 8:30AM to 5PM, and Saturday, 12PM to 3PM.