One of the first questions veterans ask when thinking about buying or building a home is how much they can actually borrow. The good news is that VA loans have no official maximum loan amount for veterans with full entitlement. What limits your borrowing power is your income, your existing debts, and what your lender approves.

This guide breaks down exactly how VA loan affordability works, what factors lenders look at, and how to figure out a realistic number before you start shopping.

If you are thinking about building rather than buying, Builders Group Construction is a VA-approved builder in Dayton that works with veterans to make the most of their VA benefit from day one. Call 937-800-4409 to connect with our team.

Is There a Maximum VA Loan Amount?

Full Entitlement Rules

Veterans with full entitlement face no VA-imposed loan limit. Full entitlement means you have never used your VA benefit before, or you used it previously and the loan has been paid off and entitlement restored.

With full entitlement, the VA guarantees 25% of whatever the lender approves. That guarantee allows lenders to offer zero down payment financing at competitive rates without a program-level cap on the loan size. For a full breakdown of how entitlement works, see our VA entitlement explained guide.

Reduced Entitlement and Loan Limits

Reduced entitlement happens when you currently have an active VA loan or previously used your benefit and did not restore it. In this case, your zero-down borrowing power is limited by your remaining entitlement and the conforming loan limits for your county.

If you want to borrow above your remaining entitlement, a down payment is required to cover the gap. This doesn’t disqualify you. It just means the zero-down benefit only extends up to your entitlement coverage.

High-Cost Area Limits

In standard counties, the 2026 conforming loan limit is $806,500. High-cost areas can go up to $1,209,750. Dayton, Ohio falls within standard county limits, which means those are the benchmarks that apply when reduced entitlement is a factor.

With full entitlement, these limits don’t restrict your loan size. Your lender’s underwriting does.

How Lenders Calculate VA Loan Affordability

Gross Monthly Income

Lenders start with your gross monthly income, meaning your income before taxes and deductions. For active duty service members, Basic Allowance for Housing, or BAH, can also count as income. Other allowances like flight pay, hazard pay, and imminent danger pay may also be included depending on the lender.

Self-employed veterans typically need to show two years of tax returns, and lenders average those figures to determine qualifying income.

Debt-to-Income Ratio

Your debt-to-income ratio, or DTI, compares your total monthly debt payments to your gross monthly income. The VA uses 41% as a general benchmark. Going above that doesn’t automatically disqualify you, but it triggers closer review of your overall financial picture.

Debts that count toward DTI include car loans, student loans, minimum credit card payments, and any other recurring monthly obligations. Expenses like groceries, utilities, and phone bills are not included in the DTI calculation.

Here is a simple example:

| Item | Monthly Amount |

| Gross monthly income | $7,000 |

| Car payment | $400 |

| Student loan | $250 |

| New mortgage payment | $1,800 |

| Total monthly debts | $2,450 |

| DTI ratio | 35% |

At 35% DTI, this borrower is comfortably within the benchmark. At 41% DTI on $7,000 gross income, total monthly debts could reach $2,870 before triggering additional scrutiny.

Residual Income Requirements

Residual income is the most unique part of VA underwriting. It measures the money left over each month after all major expenses, including the new mortgage, taxes, insurance, and existing debts, are paid.

The VA sets regional thresholds based on family size. Veterans in the Midwest, where Dayton is located, follow the Northeast region standards. Here is a simplified version:

| Family Size | Residual Income Required (Midwest) |

| 1 person | $390 per month |

| 2 people | $654 per month |

| 3 people | $788 per month |

| 4 people | $888 per month |

| 5 people | $921 per month |

Exceeding the threshold by 20% or more is a strong compensating factor that can offset a higher DTI or marginal credit score. Residual income is a major reason VA loans have historically had lower default rates than other mortgage products.

What Is the 41% DTI Rule for VA Loans?

The 41% DTI benchmark is not a hard cutoff. It is a guideline. Files above 41% are not automatically denied. They receive closer attention and may require stronger compensating factors like higher residual income, significant cash reserves, or a lower credit risk profile overall.

Some lenders apply overlays that set tighter DTI limits. Others are more flexible when residual income is strong. This is one reason shopping multiple VA lenders matters. A file that gets pushback at one lender may sail through at another. Our guide to the best VA construction loan lenders in Dayton covers what to look for when comparing lenders specifically for construction financing.

To understand how your DTI affects your buying power, look at it from the loan perspective. If your gross monthly income is $6,000 and you have $500 in existing monthly debts, your available DTI capacity at 41% is $2,460 total. Subtract your $500 in debts and you have roughly $1,960 available for a monthly mortgage payment including taxes and insurance.

How Residual Income Impacts Your Buying Power

Residual income is not just a qualifying hurdle. It is a real measure of whether the loan payment fits your life. If your residual income is well above the required threshold, you have a buffer that makes the loan sustainable long term. That is exactly what lenders want to see.

When residual income is tight, even a technically approvable DTI may face resistance. Lenders know that a borrower who barely meets residual income minimums is more vulnerable to financial stress.

The practical takeaway is this. Reducing your monthly debts before applying does two things. It improves your DTI ratio and it increases your residual income. Both work in your favor at the same time.

Veterans who want to understand their full qualification picture before starting the process can review our guide on how VA construction loans work for more context on how lenders evaluate these factors.

Credit Score and Borrowing Power

Your credit score doesn’t directly determine how much you can borrow, but it affects the interest rate you receive. A lower rate means a lower monthly payment, which means you can afford a higher loan amount on the same income.

Here is the impact on a $400,000 loan over 30 years:

| Credit Score Range | Approximate Rate | Monthly Payment | Total Interest |

| 740 and above | Best available | Around $2,150 | Lowest |

| 680 to 739 | Small adjustment | Around $2,200 | Moderate |

| 620 to 679 | Moderate adjustment | Around $2,300 | Higher |

| Below 620 | Significant adjustment | $2,400 or more | Much higher |

The difference between a 620 score and a 740 score can mean $150 to $200 more per month on the same loan amount. Over 30 years that adds up to tens of thousands of dollars.

If your credit score needs work before you apply, our VA loan credit score guide walks through the fastest ways to improve your score before applying.

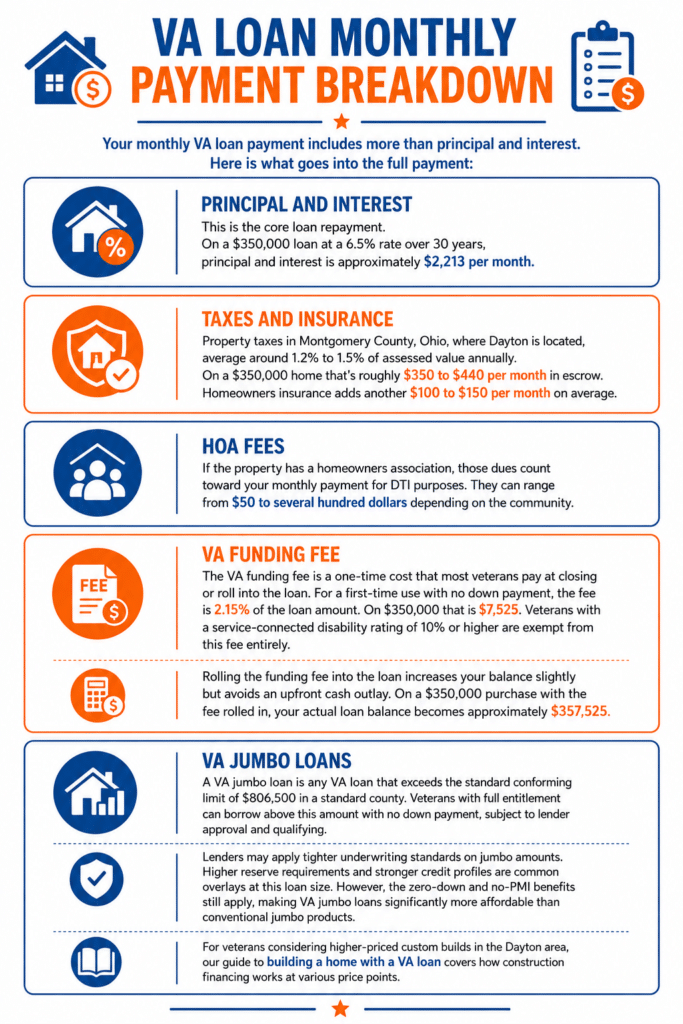

VA Loan Monthly Payment Breakdown

Your monthly VA loan payment includes more than principal and interest. Here is what goes into the full payment:

Principal and Interest

This is the core loan repayment. On a $350,000 loan at a 6.5% rate over 30 years, principal and interest is approximately $2,213 per month.

Taxes and Insurance

Property taxes in Montgomery County, Ohio, where Dayton is located, average around 1.2% to 1.5% of assessed value annually. On a $350,000 home that’s roughly $350 to $440 per month in escrow. Homeowners insurance adds another $100 to $150 per month on average.

HOA Fees

If the property has a homeowners association, those dues count toward your monthly payment for DTI purposes. They can range from $50 to several hundred dollars depending on the community.

VA Funding Fee

The VA funding fee is a one-time cost that most veterans pay at closing or roll into the loan. For a first-time use with no down payment, the fee is 2.15% of the loan amount. On $350,000 that is $7,525. Veterans with a service-connected disability rating of 10% or higher are exempt from this fee entirely.

Rolling the funding fee into the loan increases your balance slightly but avoids an upfront cash outlay. On a $350,000 purchase with the fee rolled in, your actual loan balance becomes approximately $357,525. Our guide on pros and cons of financing your home construction project covers all the cost factors worth reviewing before you commit.

VA Jumbo Loans

A VA jumbo loan is any VA loan that exceeds the standard conforming limit of $806,500 in a standard county. Veterans with full entitlement can borrow above this amount with no down payment, subject to lender approval and qualifying.

Lenders may apply tighter underwriting standards on jumbo amounts. Higher reserve requirements and stronger credit profiles are common overlays at this loan size. However, the zero-down and no-PMI benefits still apply, making VA jumbo loans significantly more affordable than conventional jumbo products.

For veterans considering higher-priced custom builds in the Dayton area, our guide to building a home with a VA loan covers how construction financing works at various price points.

Affordability Scenarios by Income

Example 1: $80,000 Annual Income

| Item | Amount |

| Gross monthly income | $6,667 |

| Existing monthly debts | $400 |

| Available for mortgage at 41% DTI | $2,333 |

| Estimated taxes and insurance | $500 |

| Available for principal and interest | $1,833 |

| Estimated affordable home price | Around $290,000 to $310,000 |

Example 2: $120,000 Annual Income

| Item | Amount |

| Gross monthly income | $10,000 |

| Existing monthly debts | $600 |

| Available for mortgage at 41% DTI | $3,500 |

| Estimated taxes and insurance | $600 |

| Available for principal and interest | $2,900 |

| Estimated affordable home price | Around $450,000 to $480,000 |

Example 3: High-Debt Borrower at $100,000 Income

| Item | Amount |

| Gross monthly income | $8,333 |

| Existing monthly debts | $1,500 |

| Available for mortgage at 41% DTI | $1,917 |

| Estimated taxes and insurance | $550 |

| Available for principal and interest | $1,367 |

| Estimated affordable home price | Around $210,000 to $230,000 |

The third example shows how high existing debt significantly reduces buying power. Paying down $500 per month in debts before applying would add roughly $80,000 to $90,000 in buying power on the same income.

How to Increase Your VA Loan Buying Power

Pay Down Debt

Reducing monthly debt obligations is the single most effective way to increase your buying power. Every $100 per month you eliminate in debt payments adds roughly $15,000 to $20,000 in home price capacity depending on your rate.

Focus on smaller balances first to eliminate payments entirely rather than spreading payments across multiple accounts.

Improve Your Credit Score

A higher credit score lowers your interest rate, which lowers your monthly payment, which allows you to qualify for a larger loan on the same income. Even a 20 to 30 point improvement can meaningfully change your rate.

Pay down revolving balances below 30% of each card’s limit. One billing cycle after the balance updates, your score reflects the change.

Reduce Monthly Obligations

Beyond existing debt, look at other recurring monthly commitments. Subscription services, insurance costs, and other regular expenses that show up on your bank statements can sometimes affect how lenders view your overall financial health.

Add a Co-Borrower

Adding a co-borrower with income and good credit increases your qualifying income, which increases your DTI capacity. The co-borrower doesn’t need to be a veteran. Lenders combine both borrowers’ incomes and debts for qualification purposes.

For veterans thinking about multifamily financing where rental income can also boost qualifying power, our VA loan multifamily guide covers how rental income is counted toward your qualification.

Choosing the Right Lender for Maximum Affordability

Not every lender applies the same DTI limits or residual income calculations. Some are more conservative than others. Shopping at least two or three VA lenders before committing gives you a clearer picture of how each evaluates your file.

Ask each lender for a loan estimate on the same scenario, same loan amount, same lock period, same day. Then compare the rate, the total monthly payment, and the estimated closing costs side by side.

Veterans have the right to shop lenders and compare offers without affecting their loan eligibility. Taking that extra step can save significant money over the life of the loan.

If you are ready to move forward with a build, our guide on how to choose a builder for your VA construction loan in Dayton is the next step. BGC serves veterans across the Dayton area including Beavercreek, Kettering, Centerville, Springboro, and Miamisburg.

Our VA construction loan lender guide covers what to look for specifically when financing a new build in Dayton.

Frequently Asked Questions

How much income do I need for a $500,000 home with a VA loan?

At a 6.5% rate with $500 in existing monthly debts and typical taxes and insurance, you would need roughly $9,500 to $10,000 in gross monthly income to stay near the 41% DTI benchmark. That’s approximately $115,000 to $120,000 annually.

Can I borrow over $1 million with a VA loan?

Yes, with full entitlement and lender approval. VA jumbo loans have no program-level cap. You must qualify on income, residual income, and credit. Lenders may require stronger reserves at higher loan amounts.

What is VA residual income?

Residual income is the money left each month after your mortgage, debts, taxes, and insurance are paid. The VA sets minimum thresholds by family size and region. Exceeding those thresholds improves your approval chances significantly.

Does the VA require a down payment?

In most cases, no. Veterans with full entitlement can borrow with zero down payment regardless of loan size, subject to lender approval and qualifying.

How does entitlement affect affordability?

With full entitlement, the VA imposes no loan limit and you need no down payment. With partial entitlement, your zero-down capacity is limited by remaining entitlement. You can still borrow above that limit by making a down payment to cover the gap.

Does BAH count as income for a VA loan?

Yes. Basic Allowance for Housing counts as qualifying income for active-duty service members. Other military allowances like flight pay and hazard pay may also be counted depending on your lender.

What monthly payment can I afford on a $75,000 salary?

At $75,000 annual income, your gross monthly income is $6,250. With $400 in existing debts and a 41% DTI benchmark, you have roughly $2,163 available for total monthly housing costs including taxes and insurance. That translates to a home price of approximately $270,000 to $300,000 depending on your rate and local tax rates.Ready to find out exactly how much you can borrow in Dayton? Call BGC at 937-800-4409 or visit bgcnow,us to connect with our team and start planning your build today.